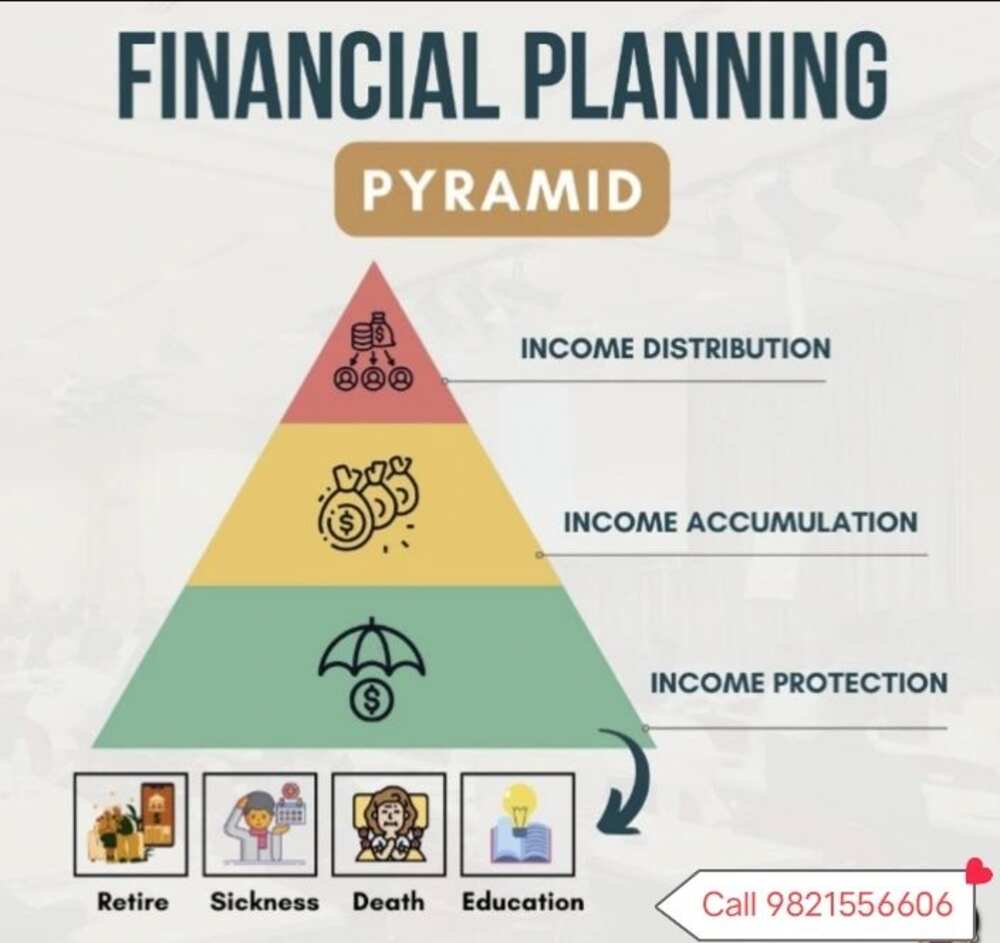

Introduction to the Financial Planning Pyramid

The financial planning pyramid is a visual framework designed to help individuals and families make informed financial decisions by structuring financial goals in a prioritized, step-by-step format. In 2025, this model is more relevant than ever as people navigate a rapidly evolving economic landscape marked by inflationary pressures, emerging technologies, and changing investment paradigms. At its core, the pyramid helps users understand what to prioritize, starting from financial security at the base and gradually building toward wealth accumulation and legacy planning at the top. This structured approach makes financial success more attainable and sustainable, ensuring individuals do not skip critical foundational steps.

Base Level: Building Financial Safety

The base of the financial planning pyramid is all about creating a financial safety net. This includes building an emergency fund, purchasing essential insurance coverage, and managing high-interest debt. A robust emergency fund, usually consisting of 3 to 6 months’ worth of living expenses, is critical. It acts as a buffer against unexpected events such as job loss, medical emergencies, or car repairs. Without it, individuals often fall into a debt cycle.

Insurance is another foundational element. Health insurance protects against medical costs, life insurance provides for dependents, and property insurance shields assets like homes and vehicles. Without adequate coverage, one unexpected event could wipe out years of financial progress.

You might also like

Managing debt, particularly high-interest debt like credit cards, is also a priority. Paying down these debts frees up cash flow, reduces stress, and improves credit scores, all of which are essential for future financial steps. Budgeting plays a key role in this stage, helping individuals control spending, identify savings opportunities, and make informed decisions.

Second Level: Financial Stability Strategies

Once a safety net is in place, the next step in the financial planning pyramid is achieving financial stability. This involves improving credit health, establishing consistent savings habits, and automating finances. Good credit not only leads to lower interest rates on loans but also opens doors to better housing and employment opportunities.

Savings should go beyond the emergency fund. Short-term goals like vacations, new appliances, or educational expenses should be planned through dedicated savings accounts. Automating savings ensures consistency, while automating bill payments helps avoid late fees and protects credit scores.

Another vital component of this level is understanding and managing financial obligations such as student loans, car loans, and mortgages. Timely payments and strategic refinancing can reduce the financial burden and open up new opportunities for investment.

Middle Tier: Long-Term Wealth Creation

The middle of the financial planning pyramid is where individuals begin to focus on wealth accumulation through investing. Diversifying investments across asset classes such as stocks, bonds, mutual funds, and ETFs helps spread risk and improve the chances of solid returns over time.

Retirement planning is a central part of this tier. Accounts like 401(k)s, IRAs, and Roth IRAs offer tax advantages and are essential for long-term financial security. Starting early allows compounding interest to work in your favor, significantly growing your retirement nest egg.

Additionally, setting long-term financial goals such as buying a home, starting a business, or funding children’s education provides direction and purpose. At this stage, it’s also wise to consult with financial planners or use sophisticated planning tools to model different financial scenarios and track progress.

Upper Tier: Advanced Financial Growth

As individuals move up the financial planning pyramid, they begin to explore advanced financial strategies. These include investing in real estate, launching businesses, or entering alternative markets like cryptocurrencies, private equity, or commodities. While these ventures carry higher risks, they also offer the potential for substantial returns.

Strategic tax planning becomes increasingly important at this stage. High-income earners benefit from strategies such as tax-loss harvesting, utilizing tax-deferred accounts, and structuring income to minimize liabilities. These tactics ensure that more money stays in your pocket and can be reinvested.

Professional advice is critical here. Financial advisors, CPAs, and tax specialists can offer insights that align with your goals and risk tolerance. They help ensure that you’re not only growing your wealth but doing so in a tax-efficient and legally compliant manner.

Top of the Pyramid: Legacy & Estate Planning

The pinnacle of the financial planning pyramid focuses on legacy building and estate planning. This stage is about ensuring that the wealth you’ve accumulated benefits future generations and reflects your values. Creating a will is the first step; it clarifies how your assets should be distributed and prevents legal disputes among heirs.

Setting up trusts can further protect assets, minimize estate taxes, and provide structured support for beneficiaries. Charitable giving, whether through foundations or donor-advised funds, allows individuals to leave a lasting social impact. Proper legacy planning also involves educating heirs about managing wealth responsibly.

Estate planning isn’t just for the wealthy. Anyone with dependents, property, or specific wishes for asset distribution should take this step seriously. It provides peace of mind and ensures that your financial goals are honored beyond your lifetime.

Modern Tools for Financial Planning (2025 Trends)

In 2025, the financial planning pyramid is more dynamic thanks to advancements in financial technology. AI-driven budgeting apps help users track spending, identify trends, and receive personalized saving recommendations. Robo-advisors offer low-cost, automated investment management, making advanced wealth strategies accessible to more people.

Digital dashboards allow users to view all aspects of their financial life—from savings and debts to investments and net worth—in one place. These tools not only save time but also empower individuals to make more informed decisions.

FinTech innovations have also democratized access to financial education. Platforms now offer courses, simulations, and real-time guidance, helping users navigate the complexities of the pyramid model with greater confidence.

Common Mistakes to Avoid

Many individuals make the mistake of jumping into investments without first establishing a secure foundation. Skipping foundational steps like emergency savings or insurance can backfire during economic downturns or personal emergencies. Similarly, investing heavily without diversification or proper research can lead to significant losses.

Another common error is ignoring inflation and the impact it has on savings and retirement planning. In a high-inflation environment, money loses value over time, and strategies must be adjusted accordingly. People also frequently underestimate the importance of tax planning, which can significantly erode investment returns.

Finally, failing to revisit and update financial plans is a critical oversight. Life circumstances, market conditions, and financial goals evolve. Regular reviews ensure that your plan remains aligned with your current reality.

Conclusion

The financial planning pyramid is a powerful tool for navigating the complexities of personal finance. It offers a step-by-step guide that starts with building a strong foundation and leads to sustainable wealth and meaningful legacy. By following this structured approach, individuals can avoid common pitfalls, make smarter financial decisions, and achieve long-term financial success.

In 2025, with the help of digital tools, expert advice, and disciplined planning, anyone can climb the financial pyramid. Whether you’re just starting out or looking to refine your strategy, understanding and applying the principles of the financial planning pyramid is key to a secure and prosperous future.

DoRead: What Financial Planning Skills Ultimately Enable an Individual to Do